Why Hoot HRT Doesn't Take Insurance (and How Superbills Can Help)

"Do you take my insurance?" is one of the first questions we get from almost every new patient. The honest answer is no, and we want to explain why, because the reason has to do with giving you better care, not less of it. We also want to be upfront about superbills, what they can realistically do for you, how to actually use one, and what to expect from your insurer once you submit it.

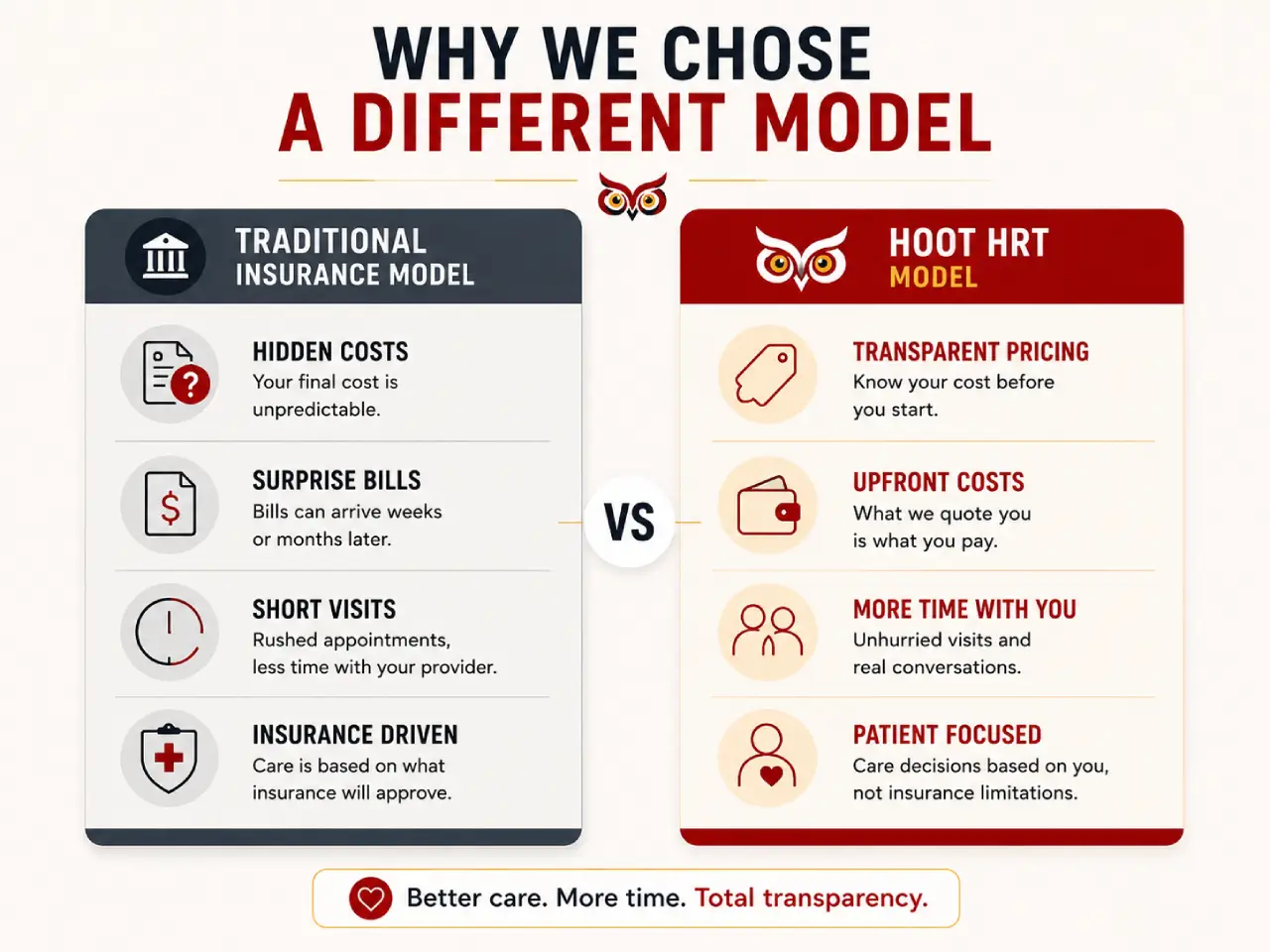

Why do we stay out of insurance billing

What a superbill actually is:

A superbill is an itemized receipt for the care you received. It typically includes the date of service, the provider's name and credentials, the diagnosis codes (ICD-10) that describe why you were seen, the procedure codes (CPT) that describe what was done, and the amount you paid. It's the same kind of documentation an in-network provider's office would normally handle internally when billing your insurance directly. The difference is that with a cash-pay clinic like ours, you receive that documentation yourself and decide what to do with it.

We give superbills to patients so you can submit them to your own insurer and pursue reimbursement on your own, if your plan allows for out-of-network claims.

To be clear about how this works: we provide the documentation, you submit it to your insurance company, and any reimbursement comes from them back to you. We're not part of that transaction, which is exactly what keeps our pricing clean and predictable on our end. We're not negotiating rates with your insurer, we're not waiting on a claims adjuster to tell us what we're allowed to charge, and we're not adjusting our care based on what a plan will or won't approve.

How to actually submit one

If you want to try for reimbursement, the general process looks like this. Check your plan's out-of-network benefits first, either through your insurer's member portal or by calling the number on the back of your card. Ask specifically about out-of-network reimbursement for the type of visit and any lab work involved. Once you have a superbill from us, you'll typically submit it through your insurer's website, mobile app, or by mail, along with any claim form they require. Many insurers process these within a few weeks, though that timeline varies a lot by carrier and by how complete the submission is. Keep a copy of everything you submit, since claims occasionally get lost or need to be resubmitted.

What might (and might not) get reimbursed

What about HSA and FSA accounts?

Many patients ask whether they can use a Health Savings Account or a Flexible Spending Account to pay for care here. In general, qualified medical expenses, including physician and clinician visits, lab work, and prescribed medications, can typically be paid for with HSA or FSA funds. The specific rules depend on your plan administrator and the IRS guidelines that apply to your account, so we'd recommend checking with your HSA or FSA administrator before your visit to confirm what's eligible under your specific plan.

An honest disclaimer

We'll give you the superbills and the documentation to give yourself the best shot at reimbursement. What we can't do is guarantee your insurance company will actually pay anything back, in part or in full. That decision sits entirely with them, based on your specific plan documents and their internal review process. What we can promise is transparency on our end, and the paperwork you need to advocate for yourself on their end. If a claim gets denied, that's a conversation between you and your insurer, and we're happy to provide any additional documentation they might request.